Property prices rose by 2.3% in 4Q 2024, largely driven by an increase of 3.4% and 3.4% in prices of non-landed properties in the RCR and OCR, respectively. Some of the new project launches in 4Q 2024 achieved benchmark prices compared to the previous quarter.

For 2024, property prices have increased by 3.9%, moderating from the 6.8% gains in 2023.

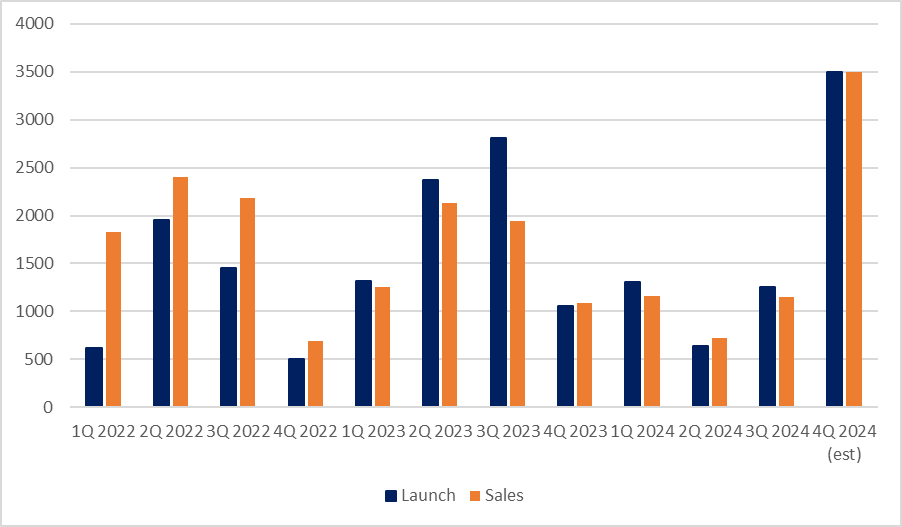

Private Homes Launch and Sales

With the interest rate cut materialising in Sep 2024, many buyers took the opportunity to reassess their borrowing limits in 4Q 2024.

Armed with a bigger loan, more buyers visited show galleries, looking for a property to buy.

Keen to ride on the positive momentum, developers pushed out more projects for sale in 4Q 2024.

Meyer Blue and Norwood Grand opened for preview in Oct 2024 while 5 projects – Chuan Park, Emerald of Katong, Nava Grove, The Collective at One Sophia and Union Square Residences held their preview in Nov 2024.

Developers are estimated to launch between 3,400 and 3,500 units in 4Q 2024. This is higher than the 3,222 units launched in the first nine months of 2024. For 2024, an estimated 6,600 to 6,700 were launched for sale, lower than the 7,551 units launched in 2023.

The projects launched in 4Q 2024 sold well on launch weekend. Emerald of Katong sold more than 99%, taking the crown of bestselling project in 2024 by units and percentage.

In 4Q 2024, an estimated 3,400 to 3,500 units are sold. This is more than the 3,049 units sold in 1Q to 3Q 2024. For 2024, more than 6,500 units are estimated to be sold, slightly more than 2023.

Figure 1: Developer’s New Sales Volume

Source: URA, Huttons Data Analytics as of 2 Jan 2025

Including ECs

The second EC project in 2024, Novo Place was launched in Nov 2024.

It attracted strong demand from first and second timers, with the 30% quota set aside for second timers fully taken up on launch day. 286 out of 504 units were sold on launch weekend. Another 137 units were sold during the second balloting in Dec 2024. It is the best-selling EC project of 2024 in terms of percentage of units sold to date.

More than 500 EC units were estimated to be sold in 4Q 2024. Together with the new private homes, more than 4,000 units were sold in the last quarter of 2024.

Purchasers’ Profile

The market dynamics has changed significantly since the imposition of 60% ABSD on foreigners buying residential properties. While Singapore remained as an attractive place to live with foreigners, the market is increasingly driven by Singaporeans.

An estimated 86.3% of purchases are by Singaporeans in 4Q 2024 compared to 82.9% in 3Q 2024. PRs made up 12.1% while foreigners accounted for 1.2% in 4Q 2024.

The proportion of purchases above $2 million has increased to 48.5% in 4Q 2024 from 41.6% in 3Q 2024. The cut in interest rate could have given buyers a bigger loan amount to purchase a slightly more expensive property in 4Q 2024.

Table 2: Comparison of Price Range and Residential Status (All Sale Types) in 4Q 2024

| <$1.5 million | $1.5 to <$2 million | $2 to <$2.5 million | $2.5 to <$5 million | $5 to <$10 million | $10 million and above | Total | |

| Singaporeans | 1,292 | 1,633 | 1,051 | 1,609 | 184 | 22 | 5,791 |

| Permanent Residents | 308 | 201 | 109 | 163 | 21 | 8 | 810 |

| Foreigners | 15 | 9 | 11 | 35 | 11 | 1 | 82 |

| Companies | 1 | – | 1 | 10 | 7 | 9 | 28 |

| Total | 1,616 | 1,843 | 1,172 | 1,817 | 223 | 40 | 6,711 |

Source: URA, Huttons Data Analytics as of 2 Jan 2025

Outlook

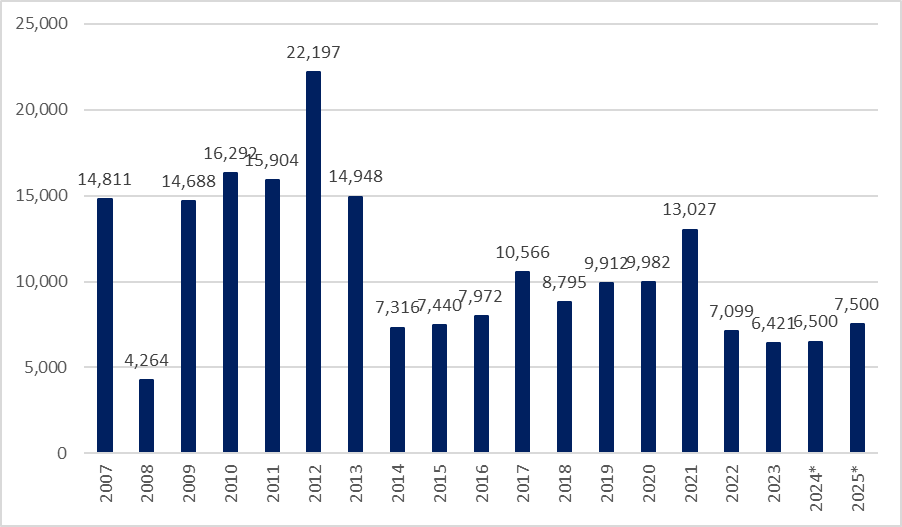

In 2025, there may be 22 launches with an estimated 11,790 units. This includes two EC launches, Aurelle of Tampines and one EC at Plantation Close.

In Jan 2025, Bagnall Haus and The Orie will be launched for sale before the Lunar New Year.

5 launches are planned for the month of Feb 2025 after the Lunar New Year. These launches are Aurea, Aurelle of Tampines (EC), Elta, Lentor Central Residences and Parktown Residence.

Huttons Data Analytics is cautiously optimistic of a better performance in the new sale market in 2025. Some of the unsatiated demand in 2024 may flow over to the launches in 1Q 2025.

Developers are estimated to sell between 7,000 and 8,000 units in 2025.

Barring unforeseen circumstances, prices in the property market are estimated to grow between 4% and 7% in 2025.

Figure 2: Developer’s New Sales Volume (2007 to 2025)

* estimates

Source: URA, Huttons Data Analytics as of 2 Jan 2025

Potential Upcoming Projects

| No. | Project Name | Developer | Location | District | Tenure | Est Units | Est Launch Period |

| 1 | Bagnall Haus | Roxy Pacific | Upper East Coast Road | 16 | FH | 113 | Jan 2025 |

| 2 | The Orie | CDL Constellation Pte. Ltd., Frasers Property Phoenix Pte. Ltd. and Sekisui House, Ltd. | Lor 1 Toa Payoh | 12 | 99 | 777 | Jan 2025 |

| 3 | Aurea | Perennial Holdings, Sino Land and Far East Organization | Beach Road | 7 | 99 | 186 | Feb 2025 |

| 4 | Aurelle of Tampines (EC) | Sim Lian Land Pte Ltd and Sim Lian Development Pte Ltd | Tampines St 62 | 18 | 99 | 760 | Feb 2025 |

| 5 | Elta | CSC Land Group (Singapore) Pte. Ltd. and MCL Land | Clementi Ave 1 | 5 | 99 | 501 | Feb 2025 |

| 6 | Lentor Central Residences | Intrepid Investments Pte. Ltd., GuocoLand (Singapore) Pte. Ltd. and CSC Land Group | Lentor Central | 26 | 99 | 475 | Feb 2025 |

| 7 | Parktown Residence | UOL-Singapore Land consortium and CapitaLand Development | Tampines Ave 11 | 18 | 99 | 1,193 | Feb 2025 |

| 8 | Arina East Residences | ZACD Group | Tanjong Rhu Road | 15 | FH | 107 | 1Q 2025 |

| 9 | Marina View Residences | IOI Properties | Marina View | 1 | 99 | 683 | 1Q 2025 |

| 10 | Marina Gardens Lane | Kingsford Huray Development, Obsidian Development and Polarix Cultural & Science Park Investment | Marina Gardens Lane | TBC | 99 | 937 | 1Q 2025 |

| 11 | Bloomsbury Residences | Qingjian Realty and Forsea Residence | Media Circle | 5 | 99 | 358 | Mar/Apr 2025 |

| 12 | Orchard Boulevard | UOL Group and Singapore Land Group | Orchard Boulevard | 9 | 99 | 270 | 2Q 2025 |

| 13 | Robertson Walk | River Valley Tower Pte Ltd | Robertson Walk | 9 | 999 | 348 | 2Q 2025 |

| 14 | Upper Thomson Road (Parcel B) | GuocoLand (Singapore) Pte. Ltd. and Intrepid Investments Pte. Ltd. | Upper Thomson Road | 26 | 99 | 941 | 2Q 2025 |

| 15 | Zion Road (Parcel A) | CDL-MFA Vega Property Pte. Ltd. and CDL-MFA Altair Property Pte. Ltd. | Zion Road | TBC | 99 | 735 | 2Q 2025 |

| 16 | Plantation Close (EC) | Hoi Hup Realty and Sunway Developments | Plantation Close | 24 | 99 | 560 | 2Q/3Q 2025 |

| 17 | Canberra Crescent | Peak Nature Pte Ltd and Huatland Development Pte. Ltd. | Canberra Crescent | 27 | 99 | 375 | 3Q 2025 |

| 18 | De Souza Avenue | SL Capital (8) Pte Ltd | De Souza Avenue | 21 | 99 | 355 | 3Q 2025 |

| 19 | Holland Drive | Holly Development Pte. Ltd. | Holland Drive | 10 | 99 | 666 | 3Q 2025 |

| 20 | River Green | Winchamp Investment Pte. Ltd. | River Valley Green | 9 | 99 | 380 | 3Q 2025 |

| 21 | Margaret Drive | Intrepid Investments Pte. Ltd., Hong Realty (Private) Limited and GuocoLand (Singapore) Pte. Ltd. | Margaret Drive | 3 | 99 | 460 | 4Q 2025 |

| 22 | Zion Road (Parcel B) | Valerian Residential Pte. Ltd. | Zion Road | TBC | 99 | 610 | 4Q 2025 |

| Total | 11,790 |

* in alphabetical order followed by chronological order

Source: URA, Huttons Data Analytics as of 2 Jan 2025