Launches and Sales

After the Lunar Seventh Month lull in Aug 2024, developers’ sales jumped 90.0% in Sep 2024 to 401 units and 84.8% year-on-year.

This was largely due to the resumption of launches.

Developers launched 437 units for sale in Sep 2024, 60.7% higher than Aug 2024 and 542.6% higher than Sep 2023.

The first launch after the Lunar Seventh Month, 8@BT sold more than 50% on launch weekend.

The design of all the units in 8@BT are well-thought through. The 1- and 2-bedroom unit layouts are highly efficient with minimal corridor and no balcony. The landscape layout of the living and dining areas for all units further add to the appeal.

When the product is right with good finishes, buyers are willing to pay a premium for this unique product.

This was another strong showing of demand in the wider market and in the Bukit Timah micro-market. In Jul 2024, Kassia also sold more than 50% on launch weekend as well. The earlier launches in Bukit Timah, The Linq @ Beauty World and The Reserve Residences also sold very well on launch weekend.

It may indicate a gradual return in buyer’s confidence, boosted by better economic news and interest rate cuts.

Top Projects by Sales in Sep 2024

|

Project Name |

Region |

Units Sold in the Month |

Median Price ($psf) |

Lowest Price ($psf) |

Highest Price ($psf) |

|

8@BT |

RCR |

83 |

2,727 |

2,527 |

3,033 |

|

PINETREE HILL |

RCR |

72 |

2,501 |

2,156 |

2,751 |

|

HILLHAVEN |

OCR |

46 |

2,120 |

1,934 |

2,345 |

|

TEMBUSU GRAND |

RCR |

32 |

2,431 |

2,300 |

2,725 |

|

HILLOCK GREEN |

OCR |

22 |

2,224 |

2,032 |

2,555 |

|

LENTORIA |

OCR |

19 |

2,163 |

2,106 |

2,371 |

|

THE MYST |

OCR |

16 |

2,082 |

1,956 |

2,318 |

|

THE CONTINUUM |

RCR |

11 |

2,843 |

2,651 |

2,997 |

|

POLLEN COLLECTION |

OCR |

10 |

2,272 |

1,477 |

2,419 |

|

SCENECA RESIDENCE |

OCR |

10 |

2,074 |

1,923 |

2,131 |

Source: URA, Huttons Data Analytics as of 15 Oct 2024

Purchases by Market Segments and Price Range

The launch of 8@BT pushed up the proportion of sales in the RCR to 55.1% in Sep 2024.

Almost 60% of the units sold in 8@BT were priced at $2 million and below, a comfortable budget for many buyers.

It also generated more interest in RCR projects. Pinetree Hill, Tembusu Grand and The Continuum were the top selling projects in the RCR in Sep 2024.

The next best performing segment was the OCR. Projects like Hillhaven, Hillock Green, Lentoria, Sceneca Residence and The Myst offer good entry prices for buyers. About 50% of the units sold are priced at $2 million and below.

The top transaction by value in Sep 2024 was the sale of 2 units in 32 Gilstead for more than $14 million each to 2 Permanent Residents.

Singaporeans made up 90.3% of buyers in Sep 2024. This is the second highest proportion of Singaporean buyers in 2024. The proportion of Singaporean buyers is likely to stay elevated above 85% in the coming months as more buyers are considering taking up citizenship before buying.

Purchases by Residential Status and Price Range in Sep 2024

|

|

<$1.5 million |

$1.5 to <$2 million |

$2 to <$2.5 million |

$2.5 to <$5 million |

>$5 million |

Total |

|

Singaporeans |

41 |

116 |

88 |

116 |

2 |

363 |

|

Permanent Residents |

5 |

4 |

4 |

12 |

8 |

33 |

|

Foreigners |

0 |

0 |

1 |

3 |

2 |

6 |

|

Companies |

0 |

0 |

0 |

0 |

0 |

0 |

|

Total |

46 |

120 |

93 |

131 |

12 |

402 |

Source: URA, Huttons Data Analytics as of 15 Oct 2024

Purchases by Foreigners

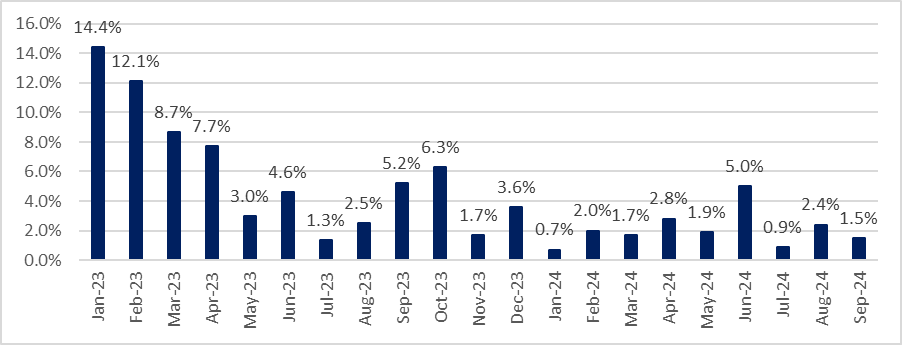

The number of purchases by foreigners in Sep 2024 was 6, similar to Aug 2024. 3 of them bought properties in the CCR while the other 3 bought in the RCR.

Proportion of Purchase by Foreigners

Source: URA, Huttons Data Analytics as of 15 Oct 2024

Executive Condominiums

Developers sold 32 EC units in Sep 2024, slightly less than Aug 2024.

Buyers were hampered by the limited choices in the market as the number of unsold EC units plunged to a record low of 171.

Outlook

Meyer Blue and Norwood Grand will book sales in Oct 2024.

Meyer Blue in East Coast, a rare and unique product which is hard to come by, sold more than 50% on launch weekend in Oct 2024.

It is the third project to sell more than 50% on launch weekend in the past few months.

Sales in the East region of Singapore have been very strong with almost 500 units sold in the past three months.

Developers’ sales in Oct 2024 are likely to exceed 500 units, much higher than Sep 2024.

The improving sales momentum comes at an opportune time as the market gears up for more launches like Chuan Park, Emerald of Katong, Nava Grove, Norwood Grand, Novo Place (EC) and Union Square Residences in the next two months.

Barring unforeseen circumstances, developers may sell up to 5,000 new homes while prices are expected to be stable, increasing up to 2% in 2024.

Potential Upcoming Projects in 4Q 2024

|

No. |

Project Name |

Developer |

Location |

District |

Tenure |

Est Units |

Month |

|

1 |

Emerald Of Katong |

Sim Lian JV (Katong) Pte Ltd |

Jalan Tembusu |

15 |

99 |

846 |

Oct 2024 |

|

2 |

Norwood Grand |

CDL Stellar Pte Ltd |

Champions Way |

25 |

99 |

348 |

Oct 2024 |

|

3 |

Chuan Park |

Chuan Park Development Pte Ltd |

Lorong Chuan |

19 |

99 |

916 |

Nov 2024 |

|

4 |

Nava Grove |

Golden Ray Edge 3 Pte Ltd |

Pine Grove |

21 |

99 |

552 |

Nov 2024 |

|

5 |

Novo Place (EC) |

Hoi Hup Sunway Jurong Pte Ltd |

Plantation Close |

24 |

99 |

508 |

Nov 2024 |

|

6 |

Union Square Residences |

CDL Libra Pte Ltd/CDL Conservo Pte Ltd/Centro Property Holding Pte Ltd |

Keng Cheow Street |

1 |

99 |

366 |

Nov 2024 |

|

7 |

Arina East Residences |

ZACD LV Development Pte Ltd |

Tanjong Rhu Road |

15 |

FH |

107 |

4Q 2024 |

|

8 |

Aurea |

GMC Property Pte Ltd |

Beach Road |

7 |

99 |

186 |

4Q 2024 |

|

9 |

Bagnall Haus |

RL Bagnall Pte Ltd |

Upper East Coast Road |

16 |

FH |

113 |

4Q 2024 |

|

10 |

Marina View Residences |

Boulevard Development Pte Ltd/Boulevard Midtown Pte Ltd |

Marina View |

1 |

99 |

683 |

4Q 2024 |

|

|

|

|

|

|

Total |

4,625 |

|

Source: URA, Huttons Data Analytics as of 15 Oct 2024